Remittance and Money Transfer: Africa Market Map

According to the latest World Bank figures, remittance payments made into sub-Saharan Africa in 2019 are estimated to have totalled $48 billion USD. A recent report published by the Brookings Institute, a research group, indicates that the volume of remittance payments in 2020 is likely to decrease as result of the global impact of the coronavirus (COVID-19) pandemic. During a time of economic uncertainty, finding an affordable means of sending money to friends and family couldn’t be more important. But has this created an opportunity for tech founders?

The World Bank estimates that in 2019 personal remittances contribute to as much as 2.77% of GDP in sub-Saharan Africa. In North Africa the contribution to GDP was higher still. In Egypt for example, personal remittance contributed 8.8% of GDP in 2019. But the cost to the consumer sending money into and within Africa are some of the highest in the World. It is estimated that sending money to the sub-Saharan Africa region costs the consumer an average of 8.9% to send $200 USD. This is considerably higher than the global average, which stands at around 6.8%.

The reason for the high cost is complex, according to 2019 report published by KNOMAD, a lack of competition in the market and high operational costs (such as ensuring compliance with stringent anti-money laundering regulations) keep prices high. But the recent raises by FinTech companies such as Chipper Cash highlight the role technology can play in creating more affordable remittance services, without sacrificing the need for necessary compliance processes.

Remittance start-ups in Africa

In November, Chipper Cash, a FinTech platform which supports intra-Africa payments, announced a $30 million Series B raise, led by Ribbit Capital with participation by Bezos Expeditions (the personal VC fund of Amazon founder, Jeff Bezos). The funding will enable the team to offer more business payment solutions, crypto-currency trading options, and investment services. Great news for the P2P payments space.

In fact, 2020 has been a big year for remittance and P2P payments companies in Africa, with companies raising $103.13 million across 8 rounds in 2020 (year to date). A big increase from the $18.63 million raised by remittance companies in 2019. Our market map highlights companies that are providing such services across Africa. A significant portion of these were headquartered in either West or South Africa, home to the five most expensive remittance corridors in Africa.

Are we missing anyone?

Are we missing anyone?

Are we missing anyone?

Are we missing anyone?Submit Startup

Is peer-to-peer remittance a viable solution?

While financial technology offers a viable alternative to expensive incumbent services, for many consumers across Africa, cash is still king. Mobile Money has long been seen as a means of providing affordable banking and payment services to those previously unable to access formal financial services. But in West Africa for example, mobile money has failed to penetrate with the same level of success seen in other parts of the continent.

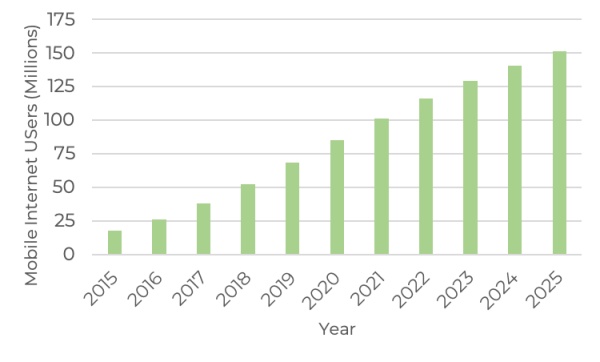

Thanks in part to expansion in Mobile coverage, GSMA, a mobile technology industry body, reports that mobile connectivity is increasing rapidly and estimates that the number of smartphone users in Nigeria will reach 144 million users by 2025. As digital adoption continues, GSMA explains, so will consumers exposure to digital financial services. Chipper Cash, for instances, reported in 2020 that they are already servicing 3 million users, processing 80,000 transactions a day.

Graph showing projected growth in Mobile penetration in Nigeria from 2015 to 2025

Source: Statista

Perhaps in response to the success achieved by FinTech companies in the remittance space, Mobile Money providers have for a long time been exploring ways to further expand their cross-border service offering. However, a recent report published by McKinsey highlights that the high cost of withdrawing cash from the Mobile Money, service compatibility and regulatory differences are still an issue for consumers. For FinTech founders, these challenges are important to bear in mind; providing truly compatible, international services could be the key to accessing the untapped potential.

Know someone helping to rebuild money transfer services in Africa? Let us know if we have missed anyone from our recruitment technology map.

For more updates, check out our LinkedIn or give us a follow on Twitter.

This article was first published in November 2020.

FREE ACCESS: Download 40 Remittance and P2P payments Technology Companies: Africa Market Map

Download Market Map

FREE ACCESS: Download 40 Remittance and P2P payments Technology Companies: Africa Market Map

Download Market Map

Contact the authors for more information about our Insight

Remittance and Money Transfer: Africa Market Map

According to the latest World Bank figures, remittance payments made into sub-Saharan Africa in 2019 are estimated to have totalled $48 billion USD. A recent report published by the Brookings Institute, a research group, indicates that the volume of remittance payments in 2020 is likely to decrease as result of the global impact of the coronavirus (COVID-19) pandemic. During a time of economic uncertainty, finding an affordable means of sending money to friends and family couldn’t be more important. But has this created an opportunity for tech founders?

The World Bank estimates that in 2019 personal remittances contribute to as much as 2.77% of GDP in sub-Saharan Africa. In North Africa the contribution to GDP was higher still. In Egypt for example, personal remittance contributed 8.8% of GDP in 2019. But the cost to the consumer sending money into and within Africa are some of the highest in the World. It is estimated that sending money to the sub-Saharan Africa region costs the consumer an average of 8.9% to send $200 USD. This is considerably higher than the global average, which stands at around 6.8%.

The reason for the high cost is complex, according to 2019 report published by KNOMAD, a lack of competition in the market and high operational costs (such as ensuring compliance with stringent anti-money laundering regulations) keep prices high. But the recent raises by FinTech companies such as Chipper Cash highlight the role technology can play in creating more affordable remittance services, without sacrificing the need for necessary compliance processes.

Remittance start-ups in Africa

In November, Chipper Cash, a FinTech platform which supports intra-Africa payments, announced a $30 million Series B raise, led by Ribbit Capital with participation by Bezos Expeditions (the personal VC fund of Amazon founder, Jeff Bezos). The funding will enable the team to offer more business payment solutions, crypto-currency trading options, and investment services. Great news for the P2P payments space.

In fact, 2020 has been a big year for remittance and P2P payments companies in Africa, with companies raising $103.13 million across 8 rounds in 2020 (year to date). A big increase from the $18.63 million raised by remittance companies in 2019. Our market map highlights companies that are providing such services across Africa. A significant portion of these were headquartered in either West or South Africa, home to the five most expensive remittance corridors in Africa.

Are we missing anyone?

Submit Startup

Is peer-to-peer remittance a viable solution?

While financial technology offers a viable alternative to expensive incumbent services, for many consumers across Africa, cash is still king. Mobile Money has long been seen as a means of providing affordable banking and payment services to those previously unable to access formal financial services. But in West Africa for example, mobile money has failed to penetrate with the same level of success seen in other parts of the continent.

Thanks in part to expansion in Mobile coverage, GSMA, a mobile technology industry body, reports that mobile connectivity is increasing rapidly and estimates that the number of smartphone users in Nigeria will reach 144 million users by 2025. As digital adoption continues, GSMA explains, so will consumers exposure to digital financial services. Chipper Cash, for instances, reported in 2020 that they are already servicing 3 million users, processing 80,000 transactions a day.

Graph showing projected growth in Mobile penetration in Nigeria from 2015 to 2025

Source: Statista

Perhaps in response to the success achieved by FinTech companies in the remittance space, Mobile Money providers have for a long time been exploring ways to further expand their cross-border service offering. However, a recent report published by McKinsey highlights that the high cost of withdrawing cash from the Mobile Money, service compatibility and regulatory differences are still an issue for consumers. For FinTech founders, these challenges are important to bear in mind; providing truly compatible, international services could be the key to accessing the untapped potential.

Know someone helping to rebuild money transfer services in Africa? Let us know if we have missed anyone from our recruitment technology map.

For more updates, check out our LinkedIn or give us a follow on Twitter.

This article was first published in November 2020.