North Africa Venture Capital – Seed Stage Market Map

The GEDI Institute gathers entrepreneurship and business statistics on a country’s entrepreneurial ecosystem through Global Entrepreneurship Index (GEI). In 2018 report (published in 2019), Tunisia ranked highest among all African nations included in the report, and 40th overall.

Morocco, Egypt and Algeria all appeared in the top 10 of African nations featured in the report. However, at the time the GEDI report was published start-ups in North Africa accounted for only 8% of Venture Capital funding closed across Africa.

Initiatives such as the Tunisian start-up act (launched in April 2018), and incubator programmes such as the Startup Launchpad announced by AUC Angels in November 2020 aim to further support a flourishing ecosystem. But for early-stage companies, has this support translated into growth?

North Africa VC Investment growth slows

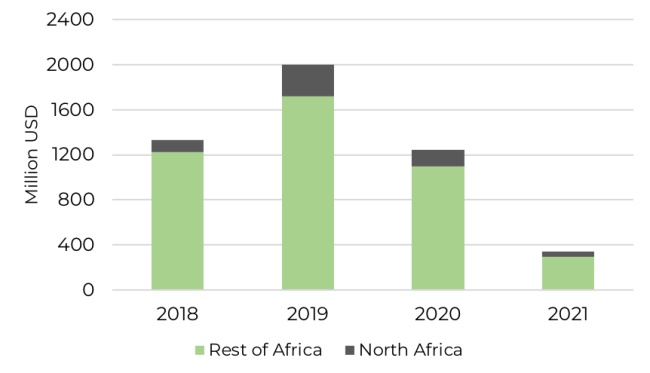

In 2018, African start-ups closed $1.331 billion USD in VC funding (excluding grants, prizes and other non-equity deals), of which start-up’s in North Africa closed $104 million USD. In 2019, the amount of funding secured by start-ups in North Africa more than doubled to $279 million USD, 14% of all venture capital funding in Africa. While funding dipped in 2020, along with broader trends across Africa, North African VC still accounted for 12% of all investment, with over $149 million USD invested.

Figure 1: Total funding secured by companies in North Africa as a proportion of funding across the rest of Africa since 2018

Source: Baobab Insights, (2021 year to date as of 05/03/2021)

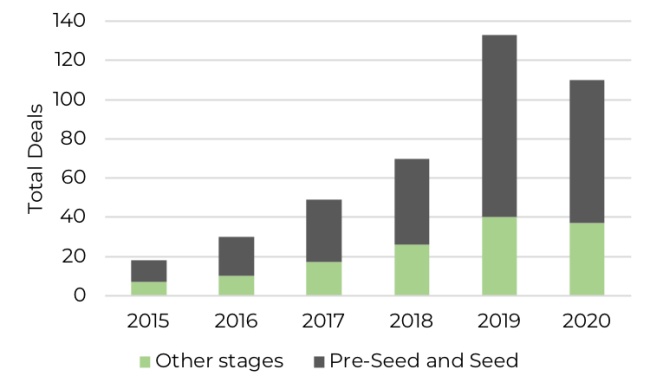

Pre-seed and seed stage investment (i.e. where the round type is stated as being Seed or Pre-Seed and funding is less than $0.550 million USD) has been growing steadily too.

In 2018, pre-seed and seed stage deals accounted for $4.3 million USD of funding across 44 deals, this grew to $8.5 million USD across 93 deals in 2019. However, while funding decreased to $7.9 million in 2020 (a 7% decrease year on year), there were only 73 such funding rounds in 2020 (a 22% decrease year on year).

Figure 2: Total Pre-seed and Seed stage deals closed by companies in North Africa since 2015

Source: Baobab Insights, (2021 year to date as of 05/03/2021)

A well supported network in North Africa

Are we missing anyone?

Submit Investor

The growing investor interest in North African VC can be attributed in part to a growing number of local VC firms that are leading the way in terms of investments.

Flat6Labs, a Egypt-headquartered VC-investor, with operations across the MENA region, disclosed 15 seed stage investments made in 2020 including Argineering, an AdTech platform based in Cairo, Dabchy, a Tunisia-based e-commerce site which helps users to resell used clothes and Brimore, an Egypt-based e-commerce focussed on artisan sellers.

212 Founders, a seed stage VC based in Morocco was also among the busiest seed stage investor in North Africa in 2020. In total they disclosed 7 investments in 2020 including Kifal Auto, a Moroccan e-commerce platform that specialises in auto-sales, Cathedis, a last mile delivery company, and Invyad, a Morocco-based FinTech that provides merchant payment services.

A different investment focus in North Africa

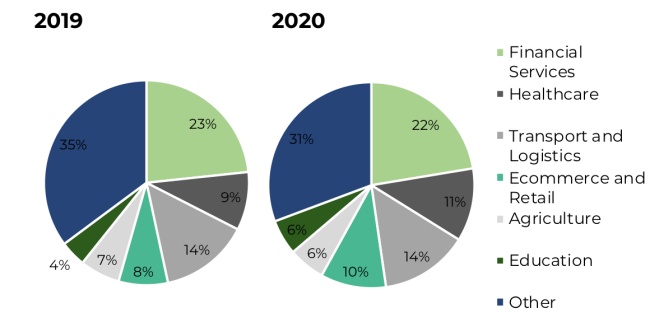

Comparing investment trends in North Africa with the rest of Africa, it is interesting to see that the types of sectors being favoured by investors are very different.

In 2020, FinTech companies across all geographies and investment stages accounted for 22% of total deals and 31% of investment raised. Despite the increased focus sectors such as e-commerce and online retail received due to the COVID-19, the number of deals increased from 8% to 10% overall (figure 3), behind Transport and Logistics (which accounted for 14% of total deals in 2020) and Healthcare (which accounted for 11% of total deals).

Figure 3: Proportion of deals closed by all start-ups across all geographies and stages in 2019 and 2020

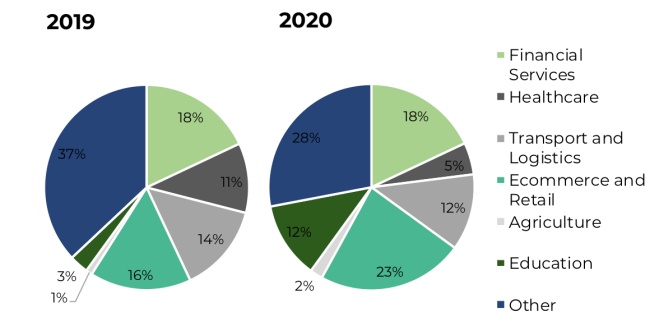

In North Africa, e-commerce and online retail companies accounted for a growing number of seed stage deals. In 2019, 16% of seed stage deals were closed by e-commerce and online retail start-ups, this grew to 23% in 2020 (figure 4). Likewise, while FinTech companies accounted for 18% of seed stage deals in both 2019 and 2020, the education sector grew the proportion of seed stage deals closed from 3% in 2019 to 12% in 2020.

Figure 4: Proportion of seed stage deals closed by North Africa companies in 2019 and 2020

What does 2021 hold for North Africa technology start-ups?

What does 2021 hold for North Africa technology start-ups?

What does 2021 hold for North Africa technology start-ups?

What does 2021 hold for North Africa technology start-ups?Mubawab, a Morocco-based PropTech announced a $10 million Venture round in March 2021, and Sakneen, which announced a $1.1. million USD Seed round with participation from Algebra Ventures, Foundation Ventures and Sarwa Capital in February. In total, start-ups in North Africa have raised $43 million in 2021 (year to date), making this a promising start to 2021.

With the continued interest globally in e-commerce, online retail and last-mile delivery technology, as well as the number of home-grown funds providing services to founders (such as the micro-VC fund announced by Cairo Angels in November 2020), hopefully we will continue to see the North Africa VC grow from strength to strength.

North Africa Venture Capital – Seed Stage Market Map

The GEDI Institute gathers entrepreneurship and business statistics on a country’s entrepreneurial ecosystem through Global Entrepreneurship Index (GEI). In 2018 report (published in 2019), Tunisia ranked highest among all African nations included in the report, and 40th overall.

Morocco, Egypt and Algeria all appeared in the top 10 of African nations featured in the report. However, at the time the GEDI report was published start-ups in North Africa accounted for only 8% of Venture Capital funding closed across Africa.

Initiatives such as the Tunisian start-up act (launched in April 2018), and incubator programmes such as the Startup Launchpad announced by AUC Angels in November 2020 aim to further support a flourishing ecosystem. But for early-stage companies, has this support translated into growth?

North Africa VC Investment growth slows

In 2018, African start-ups closed $1.331 billion USD in VC funding (excluding grants, prizes and other non-equity deals), of which start-up’s in North Africa closed $104 million USD. In 2019, the amount of funding secured by start-ups in North Africa more than doubled to $279 million USD, 14% of all venture capital funding in Africa. While funding dipped in 2020, along with broader trends across Africa, North African VC still accounted for 12% of all investment, with over $149 million USD invested.

Figure 1: Total funding secured by companies in North Africa as a proportion of funding across the rest of Africa since 2018

Source: Baobab Insights, (2021 year to date as of 05/03/2021)

Pre-seed and seed stage investment (i.e. where the round type is stated as being Seed or Pre-Seed and funding is less than $0.550 million USD) has been growing steadily too.

In 2018, pre-seed and seed stage deals accounted for $4.3 million USD of funding across 44 deals, this grew to $8.5 million USD across 93 deals in 2019. However, while funding decreased to $7.9 million in 2020 (a 7% decrease year on year), there were only 73 such funding rounds in 2020 (a 22% decrease year on year).

Figure 2: Total Pre-seed and Seed stage deals closed by companies in North Africa since 2015

Source: Baobab Insights, (2021 year to date as of 05/03/2021)

A well supported network in North Africa

Are we missing anyone?

Submit Investor

The growing investor interest in North African VC can be attributed in part to a growing number of local VC firms that are leading the way in terms of investments.

Flat6Labs, a Egypt-headquartered VC-investor, with operations across the MENA region, disclosed 15 seed stage investments made in 2020 including Argineering, an AdTech platform based in Cairo, Dabchy, a Tunisia-based e-commerce site which helps users to resell used clothes and Brimore, an Egypt-based e-commerce focussed on artisan sellers.

212 Founders, a seed stage VC based in Morocco was also among the busiest seed stage investor in North Africa in 2020. In total they disclosed 7 investments in 2020 including Kifal Auto, a Moroccan e-commerce platform that specialises in auto-sales, Cathedis, a last mile delivery company, and Invyad, a Morocco-based FinTech that provides merchant payment services.

A different investment focus in North Africa

Comparing investment trends in North Africa with the rest of Africa, it is interesting to see that the types of sectors being favoured by investors are very different.

In 2020, FinTech companies across all geographies and investment stages accounted for 22% of total deals and 31% of investment raised. Despite the increased focus sectors such as e-commerce and online retail received due to the COVID-19, the number of deals increased from 8% to 10% overall (figure 3), behind Transport and Logistics (which accounted for 14% of total deals in 2020) and Healthcare (which accounted for 11% of total deals).

Figure 3: Proportion of deals closed by all start-ups across all geographies and stages in 2019 and 2020

In North Africa, e-commerce and online retail companies accounted for a growing number of seed stage deals. In 2019, 16% of seed stage deals were closed by e-commerce and online retail start-ups, this grew to 23% in 2020 (figure 4). Likewise, while FinTech companies accounted for 18% of seed stage deals in both 2019 and 2020, the education sector grew the proportion of seed stage deals closed from 3% in 2019 to 12% in 2020.

Figure 4: Proportion of seed stage deals closed by North Africa companies in 2019 and 2020

What does 2021 hold for North Africa technology start-ups?

Mubawab, a Morocco-based PropTech announced a $10 million Venture round in March 2021, and Sakneen, which announced a $1.1. million USD Seed round with participation from Algebra Ventures, Foundation Ventures and Sarwa Capital in February. In total, start-ups in North Africa have raised $43 million in 2021 (year to date), making this a promising start to 2021.

With the continued interest globally in e-commerce, online retail and last-mile delivery technology, as well as the number of home-grown funds providing services to founders (such as the micro-VC fund announced by Cairo Angels in November 2020), hopefully we will continue to see the North Africa VC grow from strength to strength.